|

Continued from

FrontPage

of Article

THE HOTELS AND

RESTAURANTS SECTOR registered a 4.1% gain in 3Q05, compared to

5.2% in 2Q05. Steady gains in this sector reflected the continuing

strength in visitor arrivals, which rose by 8.4% in the quarter.

This bolstered occupancy rates and room revenues for hotels.

Restaurants too enjoyed a moderate increase in sales in the quarter.

GROWTH IN THE

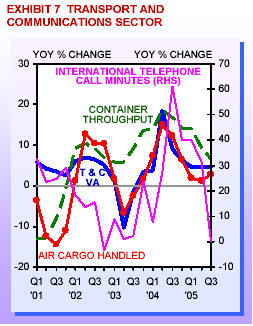

TRANSPORT AND COMMUNICATIONS SECTOR remained at 4.6% in 3Q05,

unchanged from the previous quarter. While most segments reported

stronger growth, decelerating growth in water transport and storage

services offset these gains. The air segment saw faster growth in

air cargo volumes, but a slower increase in air passenger volume.

Meanwhile, growth of the communications segment strengthened on

steady gains in both broadband and mobile phone subscriptions.

THE FINANCIAL

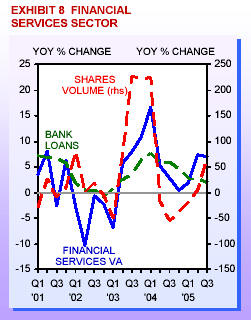

SERVICES SECTOR expanded by 7.0% in 3Q05, just a shade off the

7.3% gain a quarter earlier. During the quarter, most business

segments did better. Activity in the stock broking and fund

management segments, in particular, rose sharply compared to 2Q05.

THE BUSINESS SERVICES

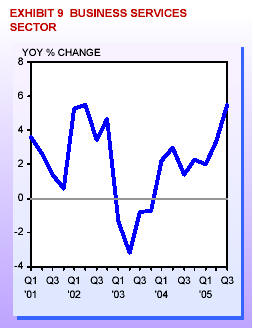

SECTOR expanded by 5.5% in 3Q05, up from 3.3% a quarter earlier.

The improvement in the sector was driven by stronger gains in the

real estate segment. Business in the segment benefited from the

strong turnaround in sentiments in recent months. Most other

business segments also registered stronger growth. Growth in the IT

services and business representative offices segments, however,

moderated slightly from relatively high rates in the previous

quarter.

Labour Market

Total employment rose by

28,700 in 3Q05, compared with 31,700 in the previous quarter. All

major industry segments registered gains, with the services segment

continuing to account for much of the increase. During the quarter,

the number of services jobs rose by 18,400. In manufacturing and

construction, the respective gains were 8,000 and 2,300.

Retrenchment, however, also rose to 2,500 from 2,116 in 2Q05 as

restructuring in the manufacturing sector hastened. The growth in

employment led to the easing of seasonally adjusted unemployment

rate to 3.3%, from 3.4% in 2Q05.

Labour Productivity

Stronger GDP growth in

3Q05 lifted labour productivity by 2.1% in the quarter, compared

with a 1.2% gain a quarter earlier. The manufacturing and wholesale

& retail trade sectors saw the largest improvement of 6.2% and 3.8%

respectively. Smaller gains were seen in the transport &

communications (1.9%) and hotels & restaurants (0.9%) sectors. The

construction, financial services as well as the business services

sectors, saw declines in labour productivity.

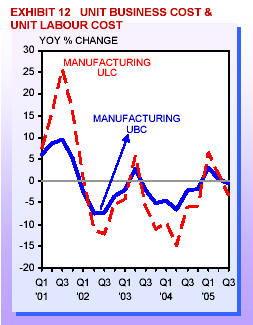

Business Costs

The overall unit labour

cost (ULC) index rose for the fourth consecutive quarter. ULC went

up by a slower 0.8% in 3Q05, compared to the 1.3% increase in the

previous quarter. The unit business cost (UBC) index of

manufacturing fell 0.7% in 3Q05, after posting 0.5% growth in the

earlier quarter. The decline was mainly due to lower manufacturing

unit labour costs. The robust growth in manufacturing output in 3Q05

had led to a 3.3% drop in manufacturing ULC, compared to the 1.6%

increase a quarter earlier. On the other hand, services cost

increased 0.6% on account of higher costs of utilities and rents.

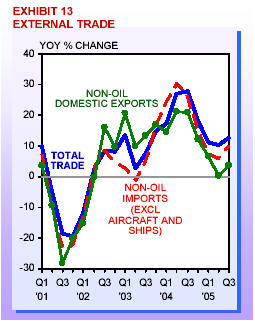

External Trade

Singapore��s external

trade expanded by 13% in 3Q05 to improve on the 10% pace set a

quarter earlier. Total exportsin the three-month period grew at

13%,also higher than the 10% in 2Q05. Both domestic exports and

re-exports registered stronger growth. In particular, NODX grew by

3.6%, up from 0.3% in 2Q05. Growth of non-oil imports (excluding

aircraft and ships) also accelerated to 10%, from 5.9% in 2Q05. In

volume terms, total trade increased by 9.1%, up from 7.2% gain in

the previous quarter.

Investment

Commitments

In 3Q05, manufacturing

investment commitments totalled $1.8 billion in terms of fixed

assets. When the commitments are fully operational, they would

create a value added of $1.6 billion and generate about 2,200 jobs.

54% would be for skilled workers. Investment commitments in services

promoted by EDB in the third quarter of 2005 amounted to $391

million in total business spending. When these commitments are

realised, they will generate a value added of close to $700 million

and create about 1,800 jobs of which 78% are for skilled workers.

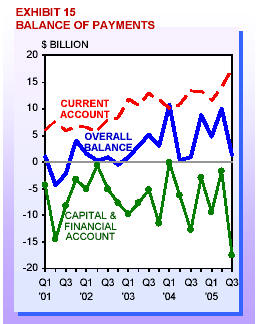

Balance of Payments

Singapore��s overall

balance of payments registered a smaller surplus of $1.3 billion in

3Q05, compared with $10 billion in 2Q05. This reflected the increase

in net outflow from the capital and financial account, even as the

current account recorded a larger surplus. The current account

balance in the quarter reached $17 billion, up from $14 billion a

quarter earlier. Net outflow from the capital and financial account

surged to $18 billion, from $1.7 billion in 2Q05. Mirroring these

developments, Singapore��s official foreign reserves in the quarter

rose to $196 billion, equivalent to 7.8 months of current imports.

Consumer Price

Inflation

The CPI rose by 0.5%

year-on-year in 3Q05, rising from 0.1% in the second quarter. Much

of the increase was accounted for by higher electricity tariff and

petrol prices. Nevertheless, lower car prices helped to keep

consumer price inflation at a relatively low rate. The impact of the

cut in foreign maid levy also continues to be reflected in the

consumer price index in the quarter.

Outlook for 2005 and 2006

The slowdown in economic growth early this year has

been more than reversed by the strength of the rebound in 2Q05 and

3Q05. This resurgence �C led by manufacturing, financial services and

entrepot trade �C mirrored the improvement in the global economy.

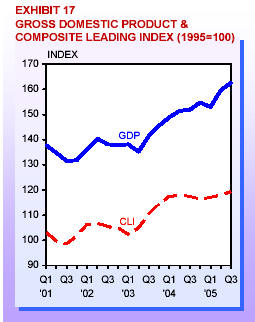

This favourable growth trend looks likely to be

sustained in the remaining months of the year. Despite the

disruptions of severe weather conditions (particularly to the oil

and natural gas industries), growth in the US is expected to remain

healthy. Easing inventory problems in the global electronics

industry is also expected to spur electronics production in

Singapore. A similar outlook is suggested by the composite leading

index for 3Q05, which registered the largest quarterly gain since

1Q04.

The latest business expectations survey continues to

show positive sentiments in all major industry segments.

Nevertheless, reflecting the strong gains already made in the past

half a year or so, this optimism has been tempered with some

caution.

For 2006, Singapore should be able to achieve its

medium term growth potential as outlook for global economy and

electronics industry remains sanguine. Growth rates in both the

developed and East Asian developing economies are forecasted to be

little changed from 2005. Global semiconductor sales growth is

expected to pick up pace in 2006. This would give a boost to

manufacturing and trade-related activities in Singapore. The

improvements in labour market conditions and the low inflationary

environment should also lift domestic demand further.

Nevertheless, risks to economic growth remain.

Limited spare capacities in the global oil industry meant that

supply disruptions would continue to send prices northwards. In the

face of rising inflation, tightening monetary conditions in the

developed economies could dampen real estate prices, which would

remove an important support for consumer demand in these economies.

Finally, should the avian flu outbreak escalate into a pandemic, it

could severely disrupt economic activities worldwide.

In view of the above considerations, the Ministry of

Trade and Industry has raised the 2005 GDP growth forecast to around

5.0%. The forecast for economic growth in 2006 is between 3.0% and

5.0%.

Annex

Source: Singapore Department of Statistics

��

Source:

www.mti.gov.sg Press Release 17 Nov

2005 ��

|