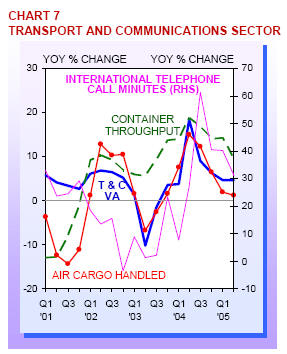

Growth In The Transport & Communications Sector clocked 4.6% in

2Q05, almost similar to the 4.7% for the previous quarter. The air

segment saw faster growth as a result of an increase in air

passenger volume. Meanwhile, the sea segment saw a moderation in

growth as container throughput and sea cargo grew at a slower rate.

Performance of the communications segment was dragged down by the

slowdown in international telephone call duration. The growth of

broadband and mobile phone subscribers, however, held steady.

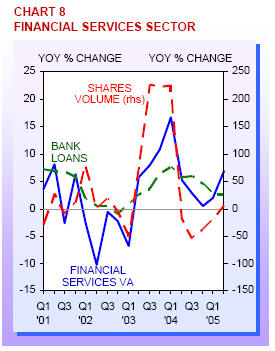

Financial Services expanded by 6.8% in 2Q05, faster than the 2.0%

growth in 1Q05. With the exception of FOREX trading, growth in all

major financial services segment improved. Growth in Asian currency

units and fund management helped drive the sector. Commercial banks,

insurance activity and stock, shares and bond brokerage also

registered a better showing this quarter.

The Business Services Sector grew by 3.1% in 2Q05, a pick-up from

the 2.1% gain in 1Q05. The expansion in the sector was driven by

continued robust performance in the business representative offices

and IT & related services. The legal and accounting segments also

grew above the sector average. Real estate activity was flat.

Labour Market

Total employment rose by 27,700 in 2Q05, larger than the 17,800

gained in the previous quarter. Both the manufacturing and services

sectors registered strong employment gains of 8,900 and 15,200

respectively. Construction employment also rose by 3,400. In 2Q05,

1,900 workers were retrenched, 12% less than in the previous

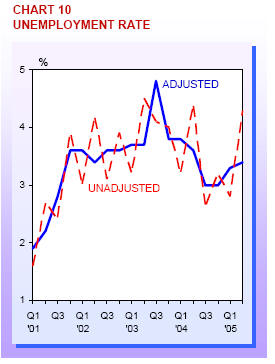

quarter. The seasonally adjusted unemployment rate rose marginally

to 3.4%.

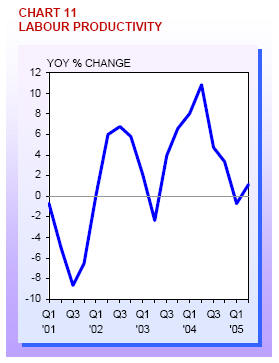

Labour Productivity Higher output growth in 2Q05 lifted labour

productivity by 1.1% in the quarter, compared with a 0.7% fall in

1Q05. Improvements were seen in industries such as wholesale &

retail trade (4.8%), transport & communications (2.3%), as well as

hotels & restaurants (2.2%).

Business Costs

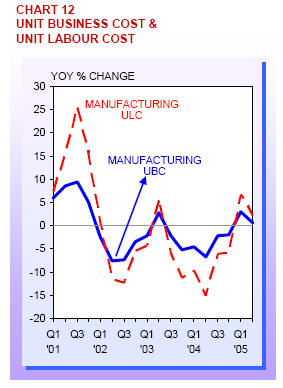

The overall unit labour cost (ULC) index inched upwards by 1.3% in

2Q05, a slower increase than the 3.5% in 1Q05. The unit business

cost index (UBC) of manufacturing crept up 0.7% in 2Q05. This was

due mainly to higher unit labour costs.

External Trade

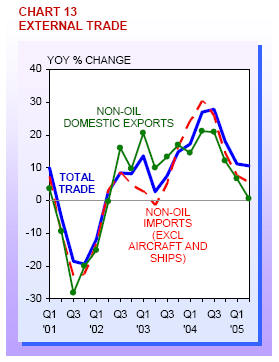

Singapore��s external trade expanded by 10.5% in 2Q05, marginally off

the 11.3% pace set in 1Q05. Similarly, total exports grew at 10.5%

in the quarter, compared with 10.7% in 1Q05. Both domestic exports

and re-exports helped to sustain growth. However, NODX grew by 0.6%,

slower than the 6.8% in 1Q05. Non-oil imports (excluding aircraft

and ships) expanded at a slower rate of 5.9%, from 7.6% in 1Q05. In

volume terms, total trade increased by 7.3%, after 10.4% rise a

quarter earlier.

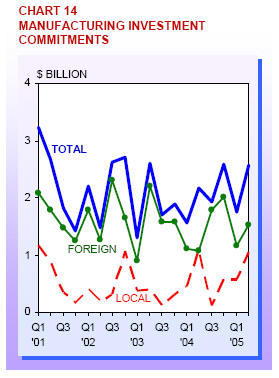

Investment Commitments

In 2Q05, manufacturing investment commitments totalled $2.6 billion

in terms of fixed assets. When realised, these investments would

create a value added of $2.2 billion and generate almost 6,300 jobs

of which 40.0% are for skilled workers. Investment commitments in

services promoted by EDB in the second quarter of 2005 amounted to

$832.9 million in total business spending. On realisation, these

investments will generate a value added of $1.6 billion and create

about 2,400 jobs of which 95.1% are meant for skilled professionals.

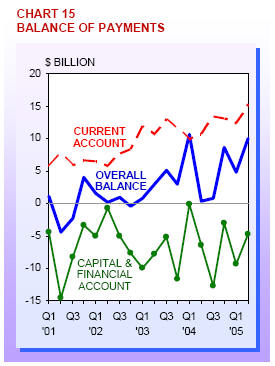

Balance of Payments

The surplus in Singapore��s overall balance of payments reached $10.0

billion in 2Q05, as a result of the decline in outflows from the

capital and financial account, as well as the improvement in the

current account surplus. The current account balance turned in a

larger surplus of $15.3 billion in 2Q05, largely due to an increase

in the goods account surplus. Against this backdrop, Singapore��s

official foreign reserves rose to $195.4 billion, equivalent to 8.0

months of current imports.

Consumer Price Inflation

The CPI rose by 0.1% in 2Q05, easing from 0.3% in the earlier

quarter. Lower housing costs contributed towards much of the

decline. Costs of education went up because of the increase in

tuition fees paid to foreign universities. An increase in the price

of recreation was largely accounted for by dearer cigarettes and

holiday travel. Transport and communications cost continued to trend

lower because of a significant decline in car prices.

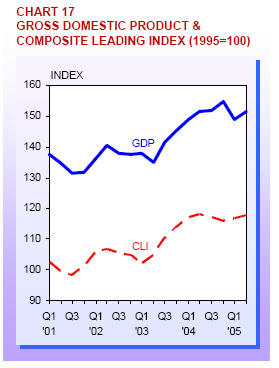

Outlook for 2005

In the first half of 2005, the Singapore economy

grew by 4.0% due to a better performance in the second quarter.

Higher second quarter growth was attributed to an expansion of

biomedical output and robust performance in key services sectors

such as wholesale & retail trade and financial services.

Moving forward, the outlook in the second half of

the year has improved. Continued growth in the G-3 economies, a

tentative recovery in the global electronics industry, limited

impact from higher oil prices and stronger domestic forward looking

indicators, together signal better prospects in the next six months.

Expectations of US economic performance in the

second half of 2005 remain optimistic on the back of healthy

expansions registered in the first two quarters. Meanwhile,

prospects for the Japanese economy in 2005 have improved. Growth in

the first quarter improved after nine months of marginal or negative

growth. This optimism was reinforced more recently by positive

readings from the June Tankan business confidence survey. In

comparison, prospects in the EU are more modest due to weak domestic

demand and a strong Euro.

In the global electronics industry, there are

tentative signs of a recovery. On the supply side, semiconductor

vendors have reduced inventories and exercised restraint in capital

spending. Meanwhile, demand for semiconductor chips is expected to

pick up in the second half of the year, particularly in niche areas

such as consumer electronics and info-communications products.

Although the pace of recovery may turn out to be slower compared to

previous electronics cycles, an improvement is still expected in the

second half of the year.

Oil prices are likely to remain high in the near

future, but its impact is expected to be tempered. Unlike the oil

shocks of the 1970s and the 1980s, which were the result of abrupt

supply disruptions, current high oil prices are due to strong growth

in two of Singapore�s major export markets ?the US and China. As long

as high oil prices are the result of strong demand, the impact on

Singapore�s economic growth should be limited.

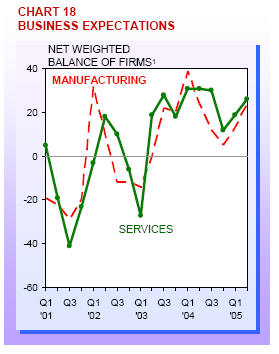

1 The y-axis of the chart on business expectations

represents the net weighted balance of companies that predict an

improvement in business situation. This is derived from the weighted

percentage of companies in the survey that predict better business

minus the weighted percentage of companies that predict worse

business.

Stronger domestic forward-looking indicators suggest that growth

momentum would continue for the rest of this year. The latest

business expectations survey reveals that sentiments in both the

manufacturing and services have improved. In view of the improved

outlook, the Ministry of Trade & Industry has narrowed the 2005 GDP

growth forecast to 3.5-4.5 per cent.